€ 55.434,21 -1,02% Today

The crypto platform you'll love

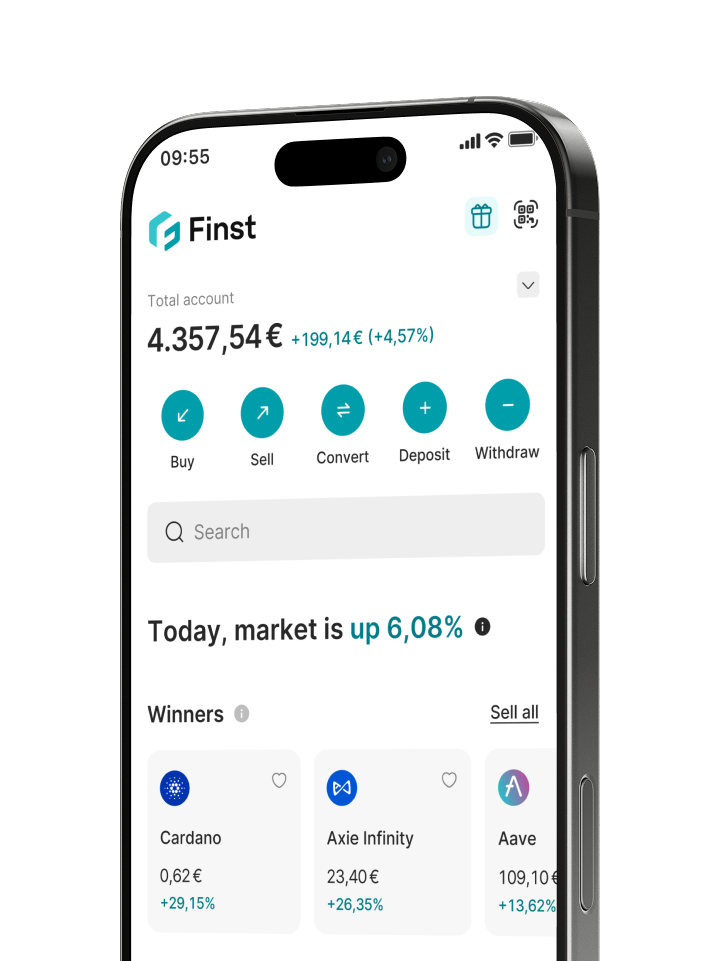

We are here to give you the tools, inspiration, and support you need to become a better investor.

Easily and securely buy Bitcoin with one of the leading crypto platforms in Europe.

Valid until 30/06.

Buy Bitcoin instantly at the best available price. Ideal for quick and easy purchases.

Set your maximum price for Bitcoin. Your order will be executed when your limit price is reached on the market

Automate your crypto purchases on a daily, weekly, bi-weekly, or monthly basis.

Create an account with a reputable crypto platform like Finst.

Deposit Euros using payment methods like iDEAL-Wero, Bancontact, or SEPA.

Buy Bitcoin and securely store it on our platform.

We are here to give you the tools, inspiration, and support you need to become a better investor.